April 2026 Newsletter

To Our Clients,

We find ourselves once again in mid-April facing a familiar feeling. Markets are unsettled, headlines are loud, and the path forward feels uncertain.

One year ago, we were in the midst of the aftermath of Liberation Day. Equity markets had just receded 20% from their previous highs, and uncertainty about the rollout of tariffs was high. Today, the concern is different, but the feeling is the same.

Now, we face renewed uncertainty stemming from the conflict in the Middle East involving the US, Israel, and Iran. Markets have responded with increased volatility, including a roughly 9% pullback from recent highs and frequent swings in both directions. The lack of progress in recent peace talks, along with the potential for a blockade of the Strait of Hormuz, suggests continued turbulence ahead.

We will be direct about this. We do not know how this conflict will unfold in the near term. No one does. But we do know something far more important. We know how markets have historically responded to events like this.

History is not just a comfort. It is evidence.

Let’s use this time to look back at major geopolitical shocks: the start of World War II, Pearl Harbor, the Cuban Missile Crisis, the Iraq War, and the Arab Oil Embargo, among others. Analysis shows that of the 17 major incidents since 1939, you will find that twelve months after the start of each conflict, the S&P 500 had a positive average return of 2.92%.

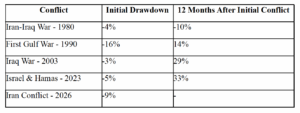

In this instance, the major concern is a prolonged spike in the price of oil and the effects it will have on inflation and the economy. Given the importance of the Middle East for oil production, let’s look specifically at other Middle East conflicts. Here, the pattern becomes even clearer:

These are not isolated outcomes. They are consistent with how markets function.

Markets are forward looking, price in fear quickly, and move on before the uncertainty is fully resolved. The recovery often begins while the headlines are still at their worst.

There will be volatility. There may be further downside. That is the cost of investing. But volatility is not risk in itself. Permanent loss of capital is.

History shows that reacting to geopolitical fear has rarely been a winning strategy.

There is always a reason to sell.

Geopolitical events dominate headlines, but over time they are not what drive long-term returns. Earnings, cash flow, and business quality ultimately determine where equity prices go. Headlines can move prices in the short term, but fundamentals determine outcomes over the long term. We are now entering earnings season, and the operating results from our investments will speak for themselves.

As always, we use volatility as an opportunity to upgrade our portfolios and buy great businesses at great prices. For instance, we recently initiated a position in Texas Instruments (TXN), the leading analog semiconductor manufacturer. The company is coming out of a six-year investment cycle, having spent $20 billion building out state-of-the-art semiconductor fabrication capacity that should drive higher volumes and improved profitability. At the same time, the analog market is emerging from a prolonged downturn and beginning to recover. The combination of a cyclical upturn and structurally improving cash flows creates a compelling opportunity.

Beyond the war, the other major force shaping markets today remains artificial intelligence. This is not a short-term theme. It is a multi-year transformation that will reshape large parts of the economy. It is clear to us that there will be winners and losers in this technological shift, the same way there has been in historical periods of technological advancement. However, the market has been slow to credit any companies as “AI-winners”, instead selling off broad baskets of companies as perceived “AI-losers”. It is in these moments of indiscriminate selling where we believe we can find excellent opportunities for long-term capital appreciation. While we expect it will still take time to work through, the winners will see substantial upside.

Periods like this also reinforce the importance of proper asset allocation. While equities have been volatile, the bond market has provided stability. Despite rising interest rates during March and the fear of inflation picking up, the broad fixed income market was essentially flat, serving its role as ballast. Because the bond market has held up well, we are not seeing significant dislocations to be taken advantage of in this market. If we do start to see bonds go “on sale” we will look to capture opportunities to inject portfolios with attractive yields where appropriate.

The breakdown in peace talks this weekend shows that this conflict will not end quickly. The longer the Strait of Hormuz remains disrupted, the greater the risk of supply chain pressure, higher energy prices, and renewed inflation concerns. This would increase the likelihood of rate increases this year and continued market volatility in the short term.

We remain patient with our capital and prepared to act as opportunities arise. Periods like this test discipline. They also create opportunity. We intend to remain on the right side of both.

We wish you a wonderful spring season.

Sincerely,

Rick Ryskalczyk, CFA

Managing Partner, Portfolio Manager

Disclosure: This newsletter is provided for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment product. The views expressed are those of Sandhill Investment Management (“Sandhill”) as of the date of publication and are subject to change without notice. References to market conditions, economic trends, securities, or investment strategies are for illustrative purposes only and do not represent a guarantee of future results. Forward-looking statements reflect current expectations and assumptions and are inherently uncertain; actual results may differ materially due to market, economic, geopolitical, and other factors. Sandhill Investment Management is a registered investment adviser with the U.S. Securities and Exchange Commission and is independently owned and operated. The Concentrated Equity Alpha Strategy is an all-cap core equity strategy that may invest in large-, mid-, and small-capitalization U.S. common stocks, American Depositary Receipts (A.D.R.s), domestic exchange-traded funds (ETFs), sector ETFs, and cash. References to specific securities, including Texas Instruments, are for illustrative purposes only, reflect current portfolio activity as of the date of this publication, and do not constitute a recommendation to buy or sell any security. Holdings are subject to change without notice. Any market or index references, including the S&P 500 Index and references to historical geopolitical event returns, are provided for general informational and illustrative purposes only. Historical market data referenced herein has been obtained from thirdparty sources believed to be reliable; however, Sandhill makes no guarantee as to its accuracy or completeness. Indices are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. For additional information or full strategy disclosures, please contact Sandhill Investment Management at 716-852-0279.