Active Management

Deploying fundamental analysis to capitalize on market inefficiencies and outperform benchmark indices.

Known as a “hands-on” style of investing, active management is the only way to successfully exceed market results. This style of investing incorporates information and knowledge gained from fundamental analysis to make informed investment decisions.

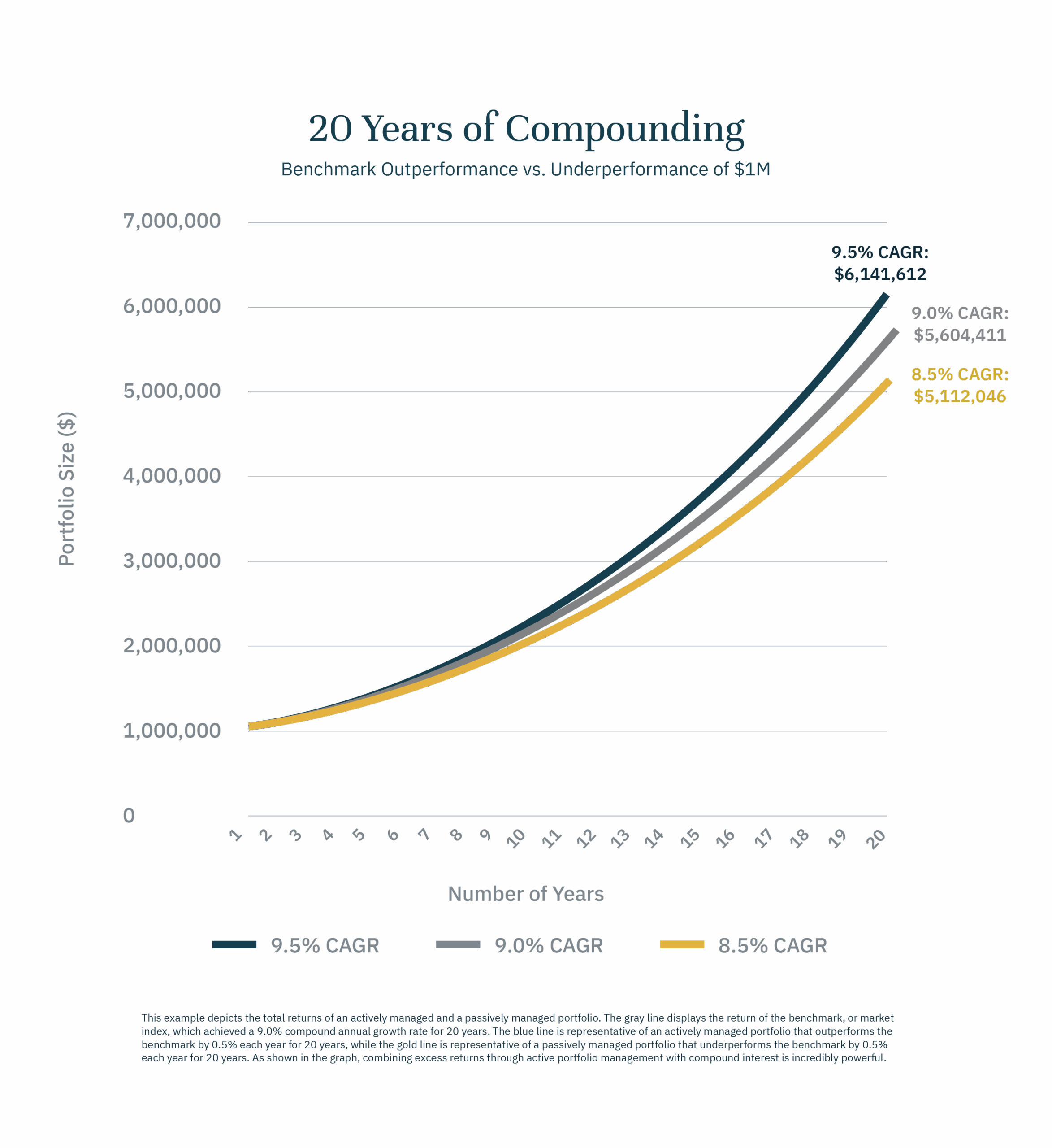

At Sandhill, we leverage the power of active management to guide our investment approach. Instead of blindly following broad indices through passive management, our research analysts use market inefficiencies to their advantage. By identifying and investing in attractively priced securities with exceptional long-term growth potential, we can generate excess returns for our clients. And when these excess returns are compounded over time, it can lead to considerable wealth creation.

Further, when comparing active management to passive strategies that inherently underperform when accounting for fees, even small differences in net-of-fee performance can generate substantial wealth differential over the long term.

Concentrated Portfolios

Maximizing investment returns by optimizing the number of stocks in our portfolio.

As the great Warren Buffett once said, “Diversification may preserve wealth, but concentration builds wealth.”

But what does it mean if an investor’s portfolio is concentrated? To put it simply, think of concentration as “quality over quantity.” Holding fewer stocks allows investors to center their focus on higher-caliber investments that can maximize potential gains.

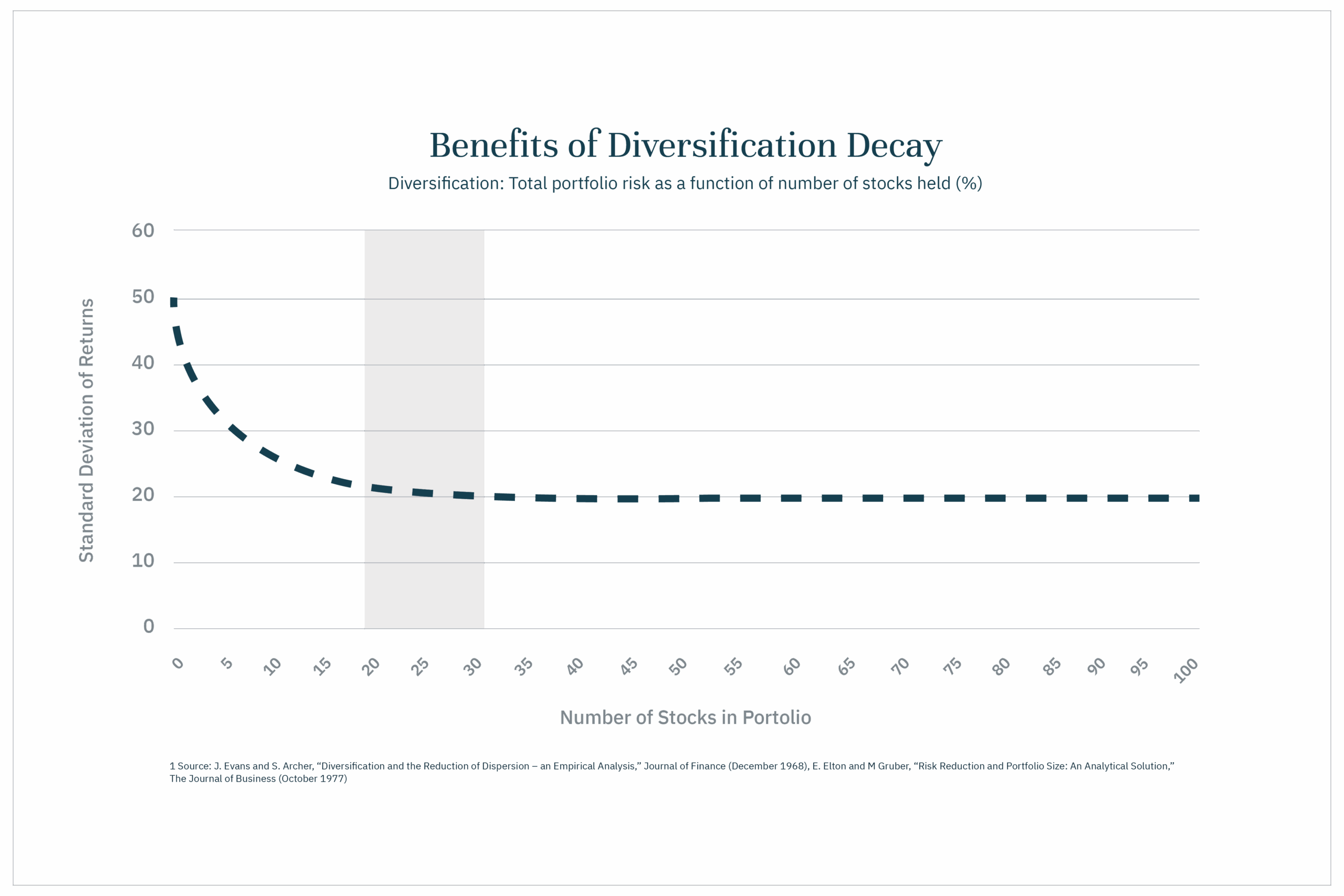

So why does it make more sense for equity portfolios to be concentrated? Studies show the benefits of diversification decay rather quickly. As seen in the following chart, overall risk reduction plateaus upon reaching a 20-30 stock portfolio. But as active share decreases, returns inherently regress to the benchmark average—a concept we like to call “diversification.”

Rather than owning hundreds of stocks in our clients’ equity portfolios, we prefer to invest in no more than 30 companies of outstanding quality. Our team understands the importance of reaping the benefits of concentration by maximizing expected returns while avoiding the perils of over-diversification.

Bottom-Up Research

Analyzing company fundamentals before evaluating broader industry trends and macro conditions.

When evaluating potential investment opportunities, our team begins conducting its initial research on the individual business. This is the crux of a bottom-up investment strategy.

From the very start of our investigative process, all work performed by our in-house Research team is deliberate and thorough. Not only do we examine a company’s earnings and overall financial standing, but we also analyze its competitive advantages, evaluate its products and technology, and screen key members of its management team. This intensive research is carried out to ensure we understand the company and are comfortable with its valuations.

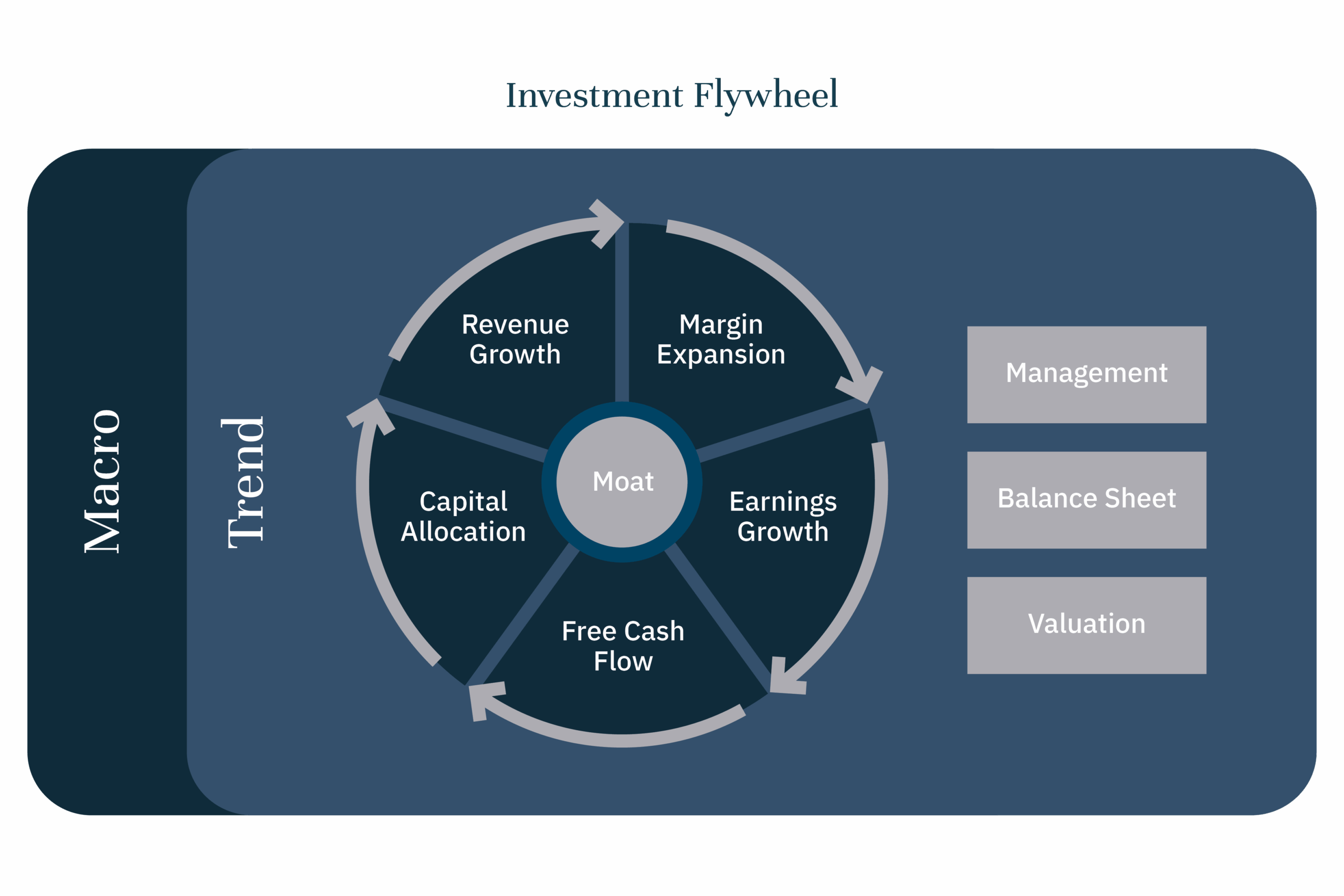

At Sandhill, we invest only in best-of-breed businesses that possess many of the positive attributes reflected in our Investment Flywheel. Through our adherence to bottom-up research, our goal is to leave no stone unturned as we search for first-rate companies that our clients can feel confident in holding for years to come.

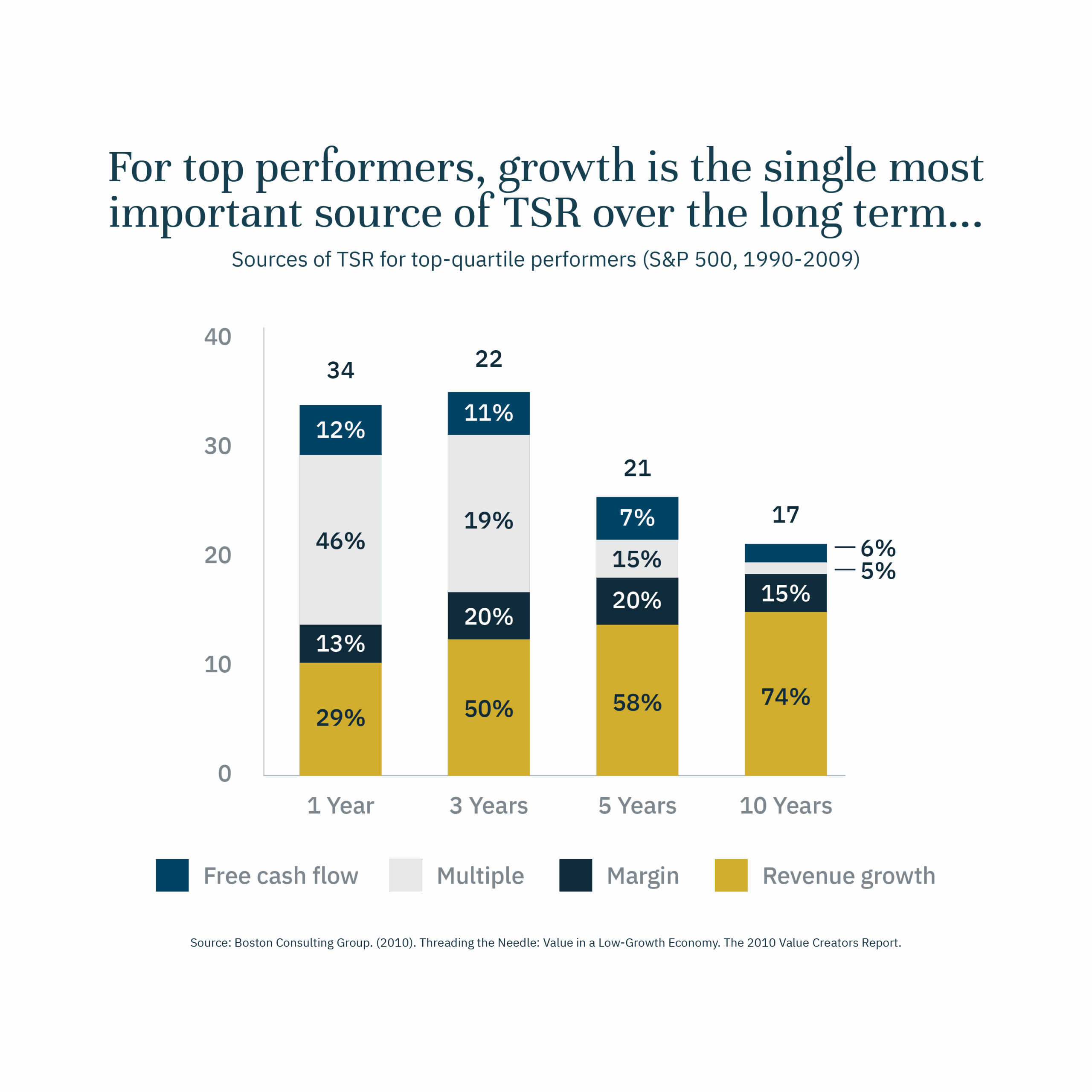

Growth-Oriented

Investing in wide-moat businesses with expanding profit margins and consistent revenue growth.

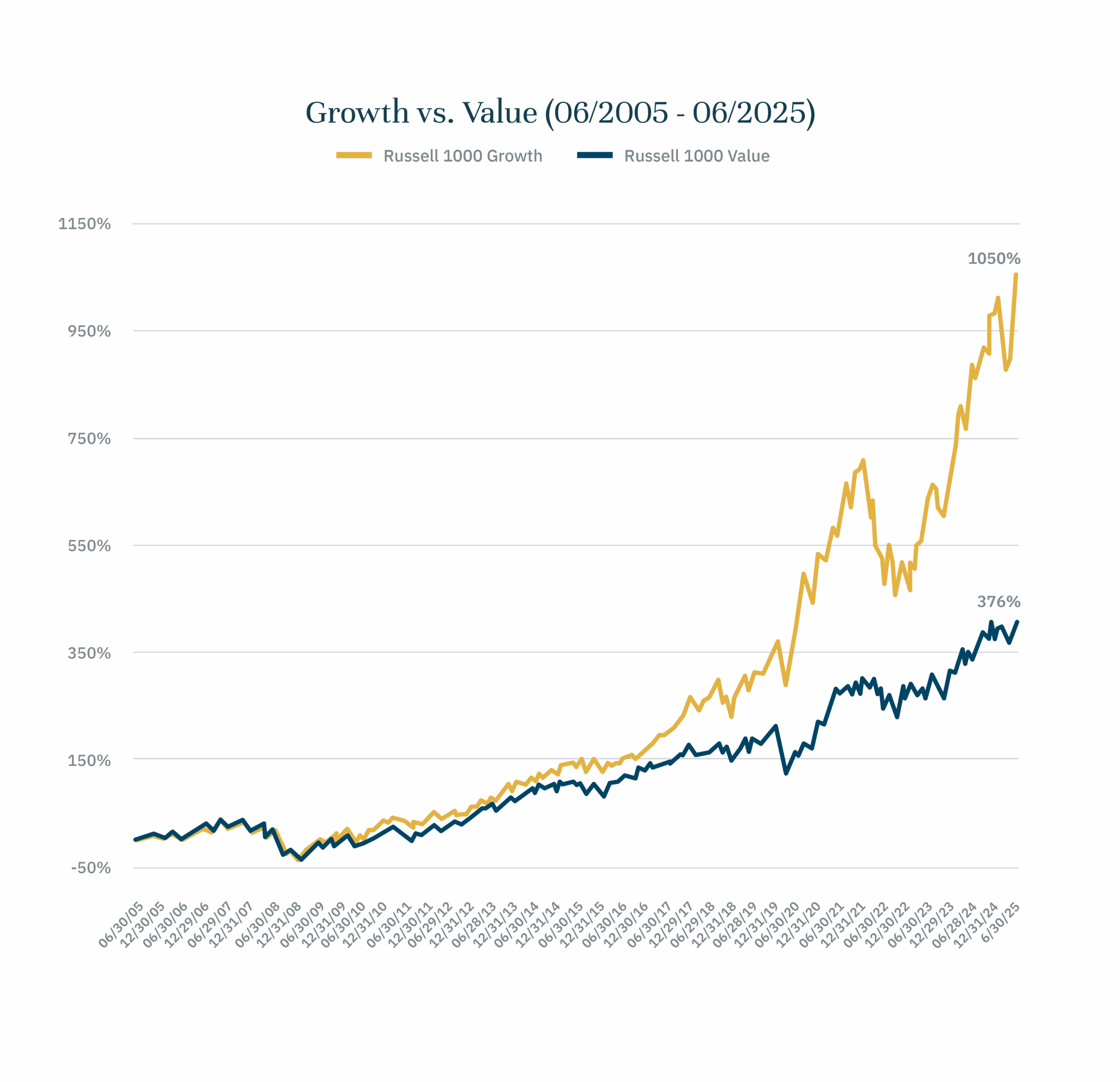

Whether you are looking over the past 5, 10, or 20 years, growth has outperformed value.

Technological advancements, innovations, and new product introductions are the driving force behind revenue growth and ultimately, value creation. Studies have shown that revenue growth is the key driver in stock performance when looking out over a multi-year time horizon.

We believe that our Investment Flywheel begins with revenue growth. Revenue growth is essential for driving margin expansion which in turn creates earnings and cash flow which when in the hands of disciplined and intelligent capital allocators ultimately leads back to further revenue growth as the flywheel spins on

Long-Term Outlook

Remaining true to our long-term investment strategy through up-and-down economic cycles.

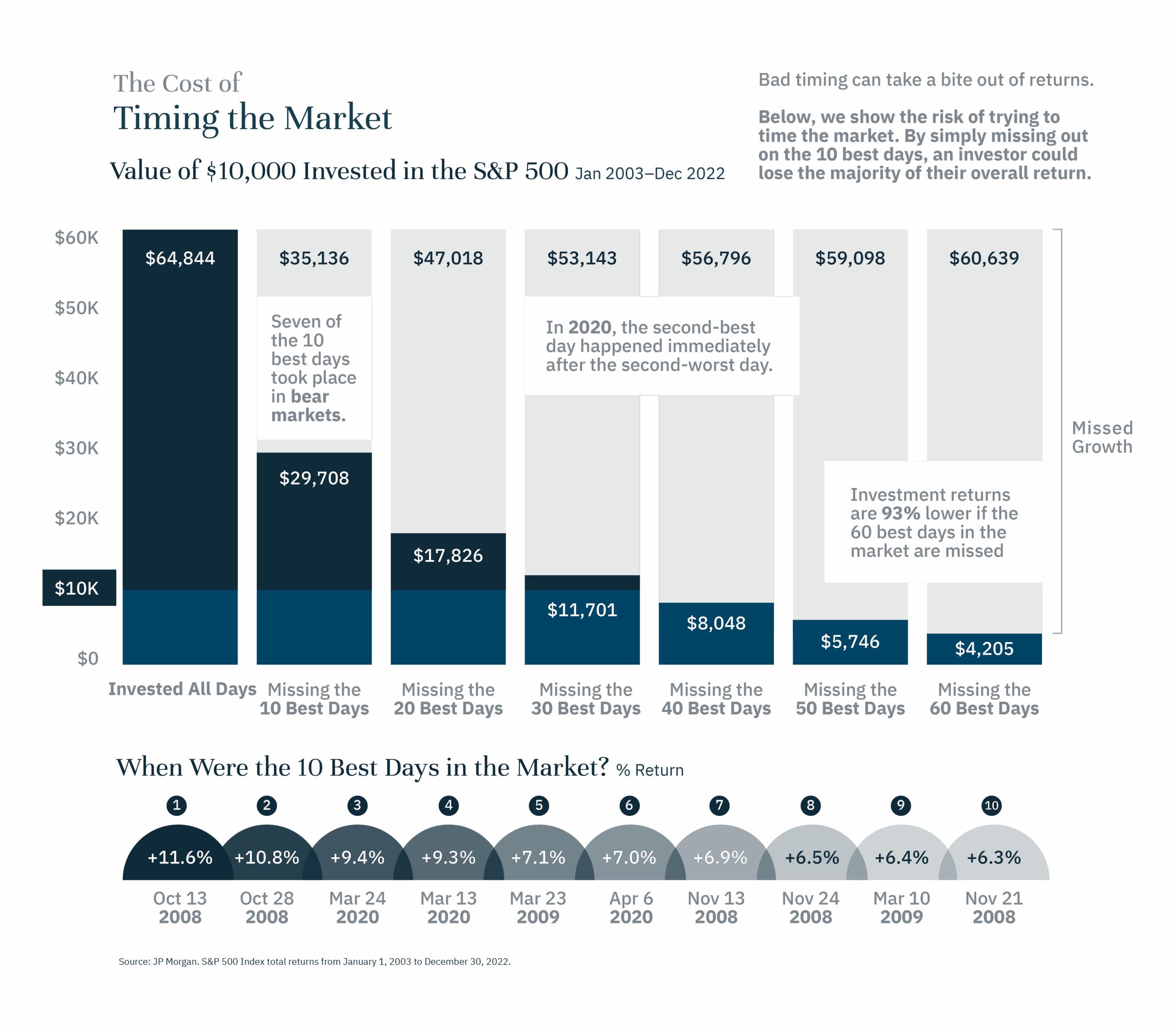

Calling short-term market movements is a fool’s game. Predicting daily, weekly, or even monthly movements in markets is nearly impossible to do accurately—and attempting to do so can be extremely costly. As demonstrated in the following visual, missing the ten best days in the market in a given year will dramatically lower an investor’s long-term returns.

Our team understands the importance of capital discipline and resisting the urge to chase after transient market trends. We are not trying to time the market by determining when peaks or bottoms will occur; instead, our objective is to invest in well-run companies through bull and bear markets.

At Sandhill, our strategies are built with resiliency in mind. While market fluctuations are common in today’s investment environment, we aim to use this volatility to our advantage by purchasing high-quality businesses at discounted prices. Discovering underpriced companies that can weather the storms of the business cycle has helped our team generate sustainable value for our clients’ portfolios.